Sign in. It’s quick, free and it’s up to you.

An account is an optional way to support the work we do. Find out more.

Sign in. It’s quick, free and it’s up to you.

An account is an optional way to support the work we do. Find out more.

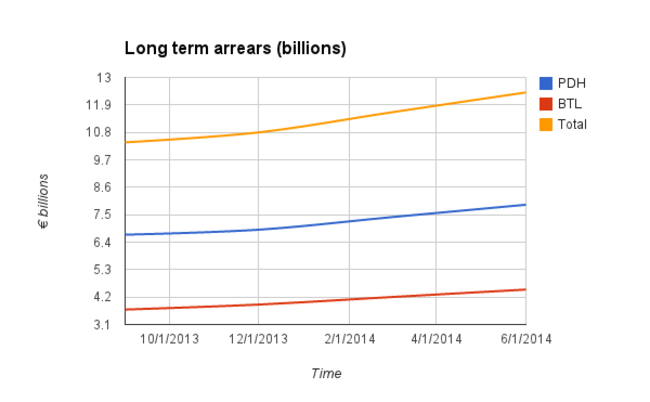

A TOTAL OF €12.5 billion in mortgages are in long term arrears of more than 720 days, a number that has been on the climb since the end of last September.

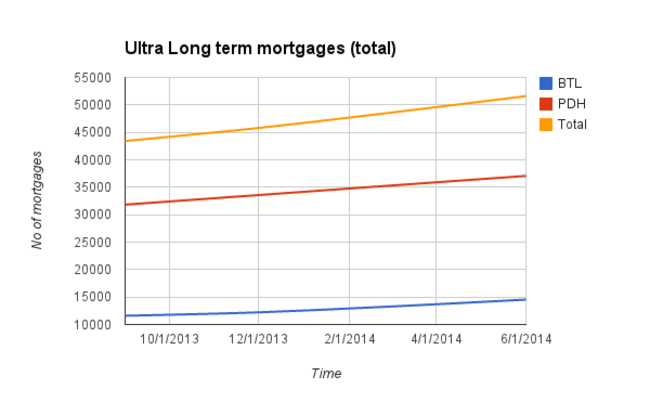

Since then, €2.1 billion of mortgages have slipped into the ultra long term arrears category between Permanent Dwellings (PDH) and Buy To Let mortgages (BTL), meaning that they are in arrears of 720 days or more.

Despite gains in the headline figures of mortgage arrears, it appears that if you’re in deep trouble servicing your mortgage, nothing the Government has done to date can help you out of it.

The banks have managed to reduce the overall level of problem mortgages, which has fallen from around €36.5 billion to around €33.6 billion, but the majority of the gains have been among customers who have fallen marginally behind on their payments.

David Hall of the Irish Mortgage Holders Association said that the Government’s strategy to tackle long term mortgage arrears is “non-existent”.

You can’t have a rate of increase at the same level for the last two years and say there’s any coherent plan at all.

He said that the targets for mortgage arrears resolution are “a complete scam and were always going to be a charade”.

On the headline figure of mortgages that are in arrears of up to 90 days, Hall questioned whether the recent reductions in the total could be due to the sale of mortgage books to non-regulated entities, which are not included in the Central Banks arrears figures.

“The 90 day figure is quite fluid and there’s a question if all those sales are included in these figures.”

Karl Deeter of Irish Mortgage Brokers said that the banks needed to consider repossessions of homes which are in long term difficulties.

“Once people go into long term arrears it tends to be a one-way journey…there’s some people where rescue plans aren’t going to work and repossessions need to happen”

He said that many of the people in arrears would have been more suitable for social housing than mortgages, but the lack of supply meant they had been forced into a credit market where standards were too loose.

The knock-on effect of the failure to repossess houses is having a profoundly destructive effect on the housing market, he argued.

Why are we so determined for people to keep houses while people in the rental sector face higher prices, other people are locked out of housing markets, while some stay in houses that they can’t afford to live in.

Noeline Blackwell, who is director general of the Free Legal Advice Centres (FLAC), said that the long-term numbers are consistent with what her organisation is encountering.

“We find that more of our contacts are from people who are in deeper difficulty, giving rise to a worry that those who became seriously over-indebted at the start of the economic crisis are not pulling out of difficulty now, but rather becoming mired more deeply.”

The total number of (PDH) mortgages in arrears has fallen to 126,005, a decline of 4.7% relative to the end of Q1.

The increase in the number of longer-term permanent dwelling home (PDH) mortgages in arrears was entirely driven by accounts in arrears of over 720 days, which rose by 1,752 and now constitute 70.3% of all arrears outstanding.

While there has been an increase in the number of PDH mortgages classified as restructured, the incidence of ‘re-default’, when a customer fails to keep up repayments on a restructured mortgage, remains high at 33.2%.

A total of 299 PDH properties were repossessed during the second quarter, while 97 Buy To Let properties were repossessed over the period, making for a total of 396 properties.

Added to the total of 354 properties taken over in the first quarter of the year, it means that 750 houses and apartments have been repossessed by the banks so far this year. This is a marked increase on the same period last year, when just 476 properties were re-possessed.

To embed this post, copy the code below on your site

have your say