Sign in. It’s quick, free and it’s up to you.

An account is an optional way to support the work we do. Find out more.

Sign in. It’s quick, free and it’s up to you.

An account is an optional way to support the work we do. Find out more.

PROGRESS ON THE auto-enrolment pension scheme is continuing, with the Government approving a general scheme of the bill to go before the Oireachtas.

Under the current timeline, the Government is seeking to have the scheme in operation by 2024, with it set to apply to approximately 750,000 workers throughout the country.

Social Protection Minister Heather Humphreys said that the General Scheme of the Automatic Enrolment (AE) Retirement Savings System Bill will now go to the Joint Oireachtas Committee on Social Protection for pre-legislative scrutiny.

“This represents a historic milestone in the journey towards enabling people who are currently without occupational pension coverage to save for their retirement,” said Humphreys on the new scheme.

“After decades of talking about Auto Enrolment in this country, I am pleased to say the AE train is now very firmly on the tracks and leaving the station ahead of its introduction in early 2024.”

While the plan itself won’t be in place for over a year, who exactly is the scheme for and how does it work?

Who is this for?

The Government has previously confirmed that the auto-enrolment scheme will apply to the approximately 750,000 workers who are between the age of 23 and 60 who are employed but are not enrolled in an occupational pension scheme.

This cohort is being targeted by the Government through the auto-enrolment scheme to allow them to begin saving for their pension earlier and to ensure that people are not left on just the State pension when they retire.

How does the scheme work?

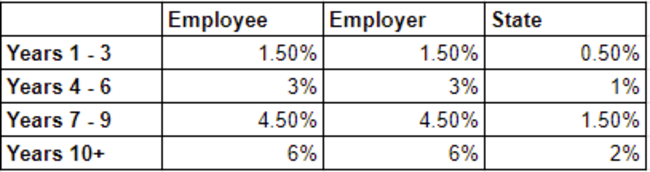

The current plan for the scheme is that employees will contribute into the pension pot, with their contributions set to be matched by their employer as a percentage of the employee’s gross income.

This contribution will then be topped up by the State.

Currently, the Government plans to phase in the contribution rates over several years, which are as follows:

So, if an employee were to pay in €3 to their pension pot, their employer must match their contribution and put in €3, while the State puts in €1.

Are pension contributions capped?

Yes and no.

Both employer and State contributions will be capped at a maximum of €80,000 of an employee’s gross annual salary.

However, employees are able to contribute on their earnings in excess of €80,000 if they wish.

Is it possible to opt-out?

While yes, people will be able to opt-out of the scheme, they cannot do so immediately.

The Social Protection Minister had previously said that anyone who is automatically enrolled in the scheme when it begins will have to wait six months until they can opt-out or suspend their contributions.

If at that point they decide to opt out, money saved by the employee may be returned to them, but both employer and State contributions will remain in the pension pot.

However, this opt-out is not indefinite, with employees being automatically re-enrolled in the scheme after two years.

Again, after being re-enrolled, employees must wait six months before they can opt out again.

Will it be possible to draw down a pension early under the new plan?

Earlier this year, it was confirmed that under most circumstances people will not be able to draw down their pension early.

Assistant Secretary General of the Department of Social Protection, Tim Duggan, previously said that the only circumstance where a person would be able to draw down their pension early was an extreme illness.

“There won’t be earlier drawdown than the retirement age for any other circumstances,” said Duggan.

By 2024, the pension age will remain at 66.

However, the Government recently approved a new “flexible” pension system which keeps the pension age at 66, but would allow people to continue working until they’re 70 in exchange for higher State pension payments.

Can you contribute lump sums?

When the new scheme is implemented, no. Humphreys has said that the current plan will be to implement the auto-enrolment scheme in full before they examine whether or not they will allow additional lump sum contributions.

Where will savings go?

The Government had previously announced that there would be four different retirement saving funds to choose from.

These four funds would have different risk/reward profiles, going from conservative, medium-risk to high-risk.

There would also be a default fund for people who prefer not to choose, which will be based on what the Department of Social Protection has called a ‘life-cycle’ investment profile.

What will happen to the State pension?

The Government has said that the State pension will remain in place despite the new proposed system, with a spokesperson for the Department calling it the “bedrock” of the new system.

To embed this post, copy the code below on your site

have your say